Payment resilience: Protecting trust, loyalty and £1.7bn of at-risk sales

DOWNLOAD FREE REPORT

10 minute read

Payment resilience: Protecting trust, loyalty and £1.7bn of at-risk sales

Retail Economics and FreedomPay surveyed UK consumers and retail and hospitality businesses to quantify the commercial impact of payment disruption in an increasingly digital-first economy.

Payment resilience has become a frontline test of customer trust. As UK consumers move decisively towards digital-first payments, tolerance for disruption is falling. Even short outages can rapidly translate into abandoned purchases, displaced spend and reputational damage.

The research estimates that payment disruption could put up to £1.7 billion of retail and hospitality sales at risk annually. While most outages are resolved relatively quickly, the financial impact escalates sharply within minutes as customers abandon transactions or switch to competitors.

The findings reveal how payment resilience is no longer purely a technology issue. It now sits at the intersection of operational execution, customer experience and commercial performance. As cash usage declines and dependence on digital payments intensifies, retailers and hospitality operators must strengthen backup capability, recovery speed and customer communication to protect loyalty and revenue.

What you can learn from this report

• How payment disruption impacts consumer trust, loyalty and purchase completion across retail and hospitality.

• Why outage duration dramatically alters lost sales risk and customer abandonment behaviour.

• Which shopping missions and customer types are least tolerant when payment systems fail.

• How declining cash usage is increasing operational and reputational exposure for businesses.

• The strategic priorities businesses need to strengthen resilience and maintain customer confidence.

Key report insights

• Payment disruption could put up to £1.7 billion of retail and hospitality sales at risk annually.

• By minute 19 of a payment outage, cumulative losses reach £932 million, representing 55% of total at-risk revenue.

• One in five consumers immediately leave without completing their intended purchase during an outage.

• 81% of UK businesses report having at least one non-cash backup payment method in place, up from 78% a year earlier.

• Only 40% of businesses offer offline card processing capability during connectivity failures.

• Over half (52%) of retail and hospitality managers have experienced verbal abuse or threatening behaviour during payment failures.

• Cash usage has fallen from nearly half of UK transactions in 2014 to below 10% in 2024.

Section 1: The commercial cost of disruption

Payment failures are becoming a major operational risk

As UK consumers become increasingly dependent on digital payments, operational resilience has become a defining commercial priority for retailers and hospitality operators. Even short periods of disruption can rapidly translate into abandoned purchases, displaced sales and reputational damage.

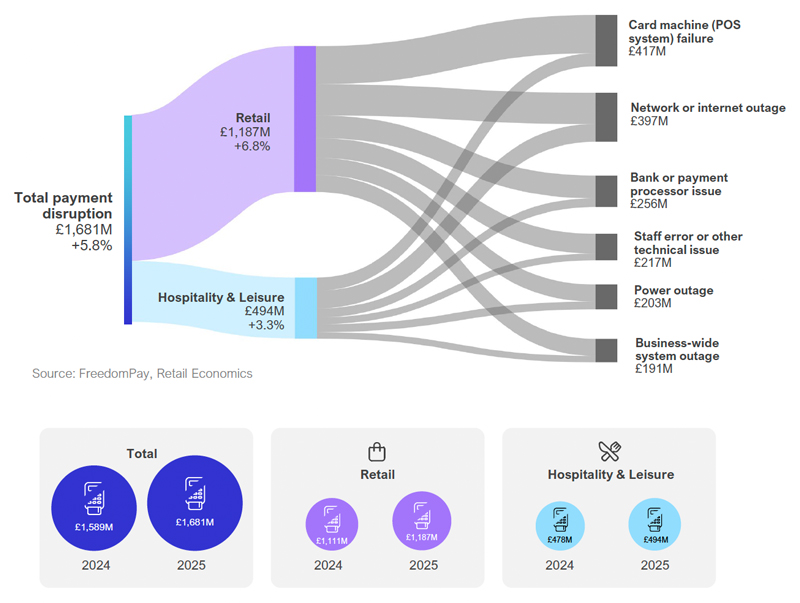

The research estimates that total payment disruption exposure has risen to £1.681 billion in 2025, up 5.8% year-on-year, with retail accounting for the majority of losses at £1.187 billion. Card machine failures and internet outages now represent the largest causes of disruption, exposing how interconnected and dependent modern payment ecosystems have become.

Figure 1 – Total payment disruption exposure and key causes of failure

Source: FreedomPay, Retail Economics

Card machine (POS) failures represent the largest single source of disruption at £417 million, followed by network or internet outages at £397 million. Payment processor failures, staff error and wider system outages also contribute significant commercial exposure across both sectors.

The findings reinforce how payment resilience can no longer be viewed as purely a technology issue. Businesses increasingly need robust contingency planning, layered infrastructure and rapid incident response capability to minimise disruption and protect customer trust.

Revenue loss escalates rapidly during outages

The commercial impact of payment disruption accelerates far faster than many businesses anticipate. While operators often assume customers will tolerate short outages, actual revenue displacement builds rapidly once queues increase and transaction confidence falls.

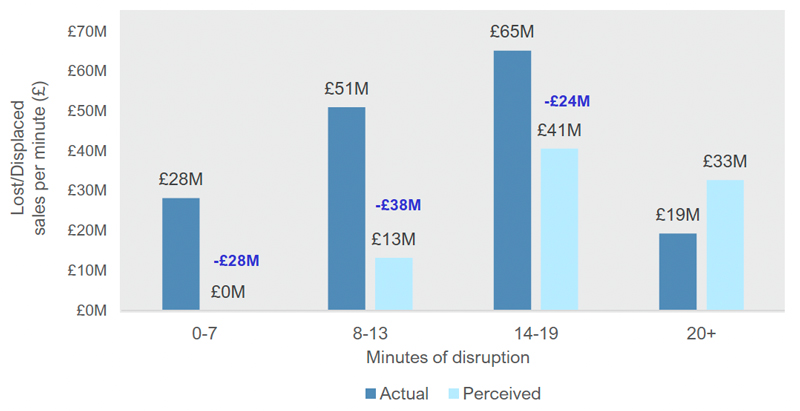

The research shows that outages lasting between 14 and 19 minutes generate actual lost or displaced sales of £65 million per minute, significantly above the perceived impact of £41 million. This expectation gap highlights how many businesses underestimate the speed at which customers abandon purchases or seek alternatives.

Figure 4 – Perception vs reality: businesses underestimate how quickly sales can be lost

Source: FreedomPay, Retail Economics

By minute 19, cumulative losses reach £932 million, representing more than half of total at-risk revenue. Beyond this point, much of the commercial damage is already locked in as customers have left stores or venues and are unlikely to return.

The findings underline the importance of rapid system recovery, offline processing capability and resilient fallback infrastructure. In an increasingly digital-first payment environment, speed of recovery has become directly linked to revenue protection.

Section 2: Consumer tolerance and behavioural response

Customer tolerance depends on mission and mindset

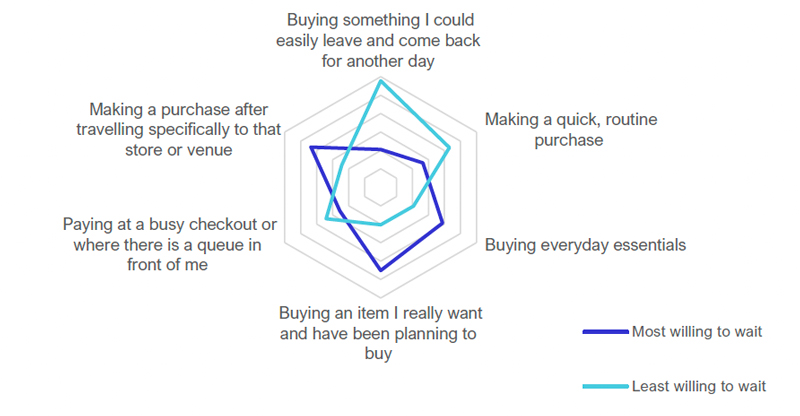

Consumer reactions to payment disruption vary sharply depending on purchase intent, shopping mission and emotional investment in the transaction. Not all outages immediately result in permanent lost sales, but tolerance levels deteriorate quickly when disruption interrupts convenience or routine.

The research shows that shoppers are most willing to wait when making planned or destination purchases, particularly after travelling specifically to a store or venue. Tolerance is far lower during quick convenience purchases or transactions consumers feel they can easily postpone.

Different customer personas create different operational risks

The research identifies four distinct consumer personas when it comes to payment disruption tolerance, ranging from highly critical digital-first shoppers to resilient cash-carrying consumers.

‘High-Risk Critics’ are affluent, digitally dependent consumers with extremely low tolerance for payment failure. Even isolated incidents can significantly reduce trust and loyalty. Meanwhile, ‘Silent Walkouts’ rarely complain but quickly abandon purchases when disruption occurs.

By contrast, ‘Cash-Ready Completers’ are generally older shoppers who maintain fallback payment options and remain relatively calm during outages. These differences highlight how payment resilience increasingly shapes customer experience and brand perception across demographic groups.

Figure 6 – Payment personas: the four main types of consumers during payment disruption

Source: FreedomPay, Retail Economics

The findings reveal how younger consumers are often the least operationally resilient during outages due to declining cash usage and higher dependency on digital payments. As payment ecosystems continue evolving, businesses increasingly need resilience strategies aligned to different customer expectations and behaviours.

Section 3: Digital dependency and resilience strategy

The shift away from cash is increasing operational exposure

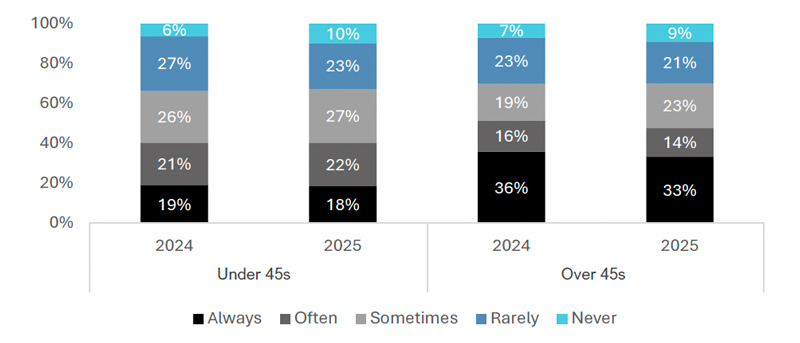

The UK has shifted decisively towards digital-first payments over the past decade, fundamentally changing the resilience requirements facing retailers and hospitality businesses. Cash usage has fallen from nearly half of UK transactions in 2014 to below 10% in 2024, while card and mobile payments now dominate.

Fewer consumers are regularly carrying cash than a year ago, reducing fallback options when systems fail. Younger shoppers are particularly exposed, with under-45s significantly less likely to carry cash compared with older generations.

Figure 8 – Fewer consumers are carrying cash, reducing fallback when systems fail

Source: FreedomPay, Retail Economics

Among under-45s, the proportion who always carry cash remains relatively low while the share who rarely or never carry cash continues to rise. Older consumers remain more likely to maintain cash as a fallback option, giving them greater resilience during payment outages.

This behavioural shift is increasing sensitivity to disruption. As digital payments become the default transaction method, reliability increasingly defines trust, meaning payment failures risk not only immediate lost sales but longer-term damage to customer confidence.

Backup resilience is improving but remains uneven

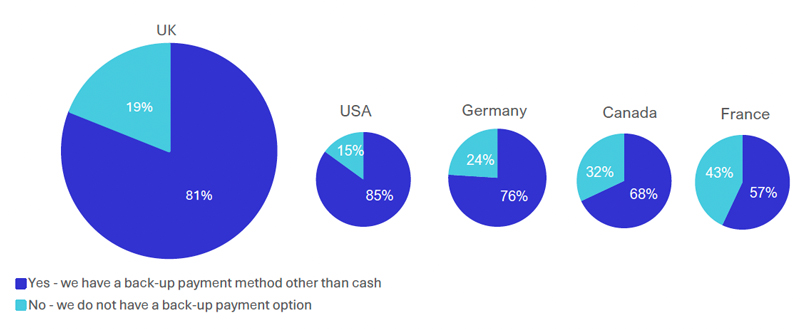

Businesses are increasingly recognising the importance of payment resilience, with backup payment adoption improving across both retail and hospitality. In the UK, 81% of businesses now report having at least one backup payment solution beyond cash.

However, resilience capability remains inconsistent beneath headline adoption figures. Many businesses still lack secondary connectivity or offline transaction processing, leaving operations vulnerable during internet outages and wider infrastructure failures.

Figure 10 – Prevalence of digital backup systems among retail and hospitality businesses

Source: FreedomPay, Retail Economics

International comparisons also reveal differing resilience maturity across markets. While the USA and UK demonstrate relatively high backup adoption levels, other markets continue to show significant gaps in fallback capability.

The findings reinforce how effective payment resilience increasingly depends on layered contingency planning. Businesses need backup systems that combine offline processing, independent connectivity and rapid recovery capability to minimise operational disruption and protect customer trust.