Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

Clothing & Footwear Sales

Clothing sales rose by xx% year-on-year in May, reversing the xx% decline recorded a year earlier. Footwear sales increased by xx%, improving on last May’s xx% fall but trailing the pace of clothing.

Clothing benefited from the shift in weather, with consumers moving into summer ranges, buying lighter layers, dresses, shorts, swimwear and holiday clothing as temperatures climbed. Footwear improved, but many shoppers updated wardrobes before committing to new shoes.

Two bank holidays added momentum. Social plans, short breaks and time spent outdoors created immediate reasons to buy, particularly during the late-May heatwave.

Key drivers

May’s heat arrived at the right point for retailers who had moved into spring and summer ranges, with the weather giving consumers a reason to act. Demand accelerated across warm-weather clothing, holidaywear and occasionwear in what was the joint third warmest May on record.

The bank holidays helped turn weather into sales. Consumers were travelling, meeting friends and spending more time outside, creating demand for outfits linked to weekends away, barbecues, festivals and early holiday preparation.

Footwear did not enjoy the same degree of uplift. Sandals and casual summer styles benefited from the weather, but the overall market remained slower.

Online channels also played an important role, allowing consumers to search for specific items, compare prices and order quickly ahead of weekend plans or holidays. This drove online sales growth to the highest level since January (+xx% YoY).

The month showed how quickly fashion demand can change when the weather improves. Apparel retailers were able to capture that shift because consumers were buying for immediate use and not just responding to lower prices.

Macro backdrop

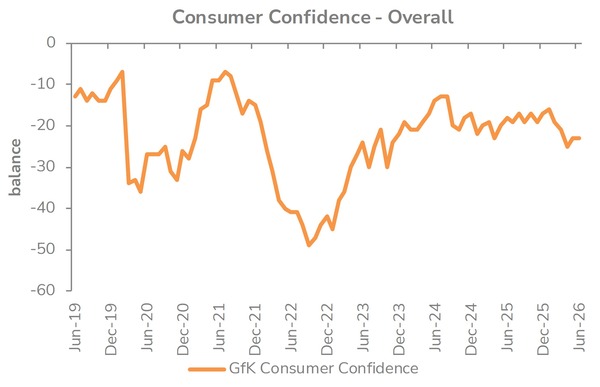

May brought some relief to household budgets. Inflation held at xx%, grocery inflation eased to a 17-month low and fuel prices fell from the highs seen earlier in the spring. Consumer confidence improved for the first time in four months, giving households more room to spend on seasonal and social purchases.

Fashion tends to respond quickly when consumers feel less pressure. Clothing purchases are easier to control than larger household commitments: a shopper can buy one item, build an outfit over time or wait for a promotion.

The wider economic picture still encouraged careful spending. The Bank of England held interest rates at xx%, mortgage rates edged higher and major purchase intentions fell to their weakest level since January 2025. These pressures were more visible in furniture and flooring than in fashion, but they kept shoppers attentive to price, promotions and perceived value.

The labour market continued to cool. Vacancies fell further; payroll employment remained below last year’s levels, and wage growth eased. Households felt more comfortable than they had earlier in the spring, but spending decisions remained closely tied to need and affordability.

Latest sector developements

A notable development came from Frasers Group’s proposed acquisition of HUGO BOSS. The group, which already owns more than xx% of the German fashion business, submitted a €xxbn (£xxbn) offer at €xx per share, sending Hugo Boss shares almost xx% higher.

Take out a FREE 30 day membership trial to read the full report.

Consumer confidence stable

Source: Retail Economics analysis, GFK

Source: Retail Economics analysis, GFK