Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Food & Grocery Sales

Food and grocery sales rose by xx% year-on-year in May, ahead of the xx% increase recorded a year earlier.

The category benefited from a favourable mix of warmer weather, two bank holidays and easing grocery inflation, all of which encouraged households to spend more on eating, entertaining and social occasions at home.

May’s heatwave changed consumers shopping behaviour. Consumers bought food for barbecues, picnics, garden gatherings and informal meals with friends and family. Seasonal ranges moved earlier, with demand rising across fresh food, drinks, snacks, confectionery and food-to-go.

The Spring Bank Holiday provided a further boost, particularly across convenience shopping missions and larger baskets linked to hosting.

Grocery remains the most essential part of household spending, but May showed consumers were prepared to add treats, premium lines and occasion-led purchases once immediate cost pressures eased.

Key trading themes and drivers

Sustained sunshine encouraged households to eat outdoors, plan weekend gatherings and shop for seasonal occasions. Barbecue food, chilled drinks, salads, desserts, snacks and convenience products all benefited as consumers made the most of the joint third warmest May on record.

Two bank holidays amplified that effect. The extra time at home created more occasions for entertaining and helped shift spend towards larger baskets.

Easing inflation also changed the mood of the weekly shop. Grocery price inflation fell to a 17-month low during May, reducing some of the pressure that had built up. Households still watched prices closely, but lower inflation gave consumers more room to trade into seasonal products and small treats.

The market remained fiercely competitive as the discounters continued to win customers through clear pricing, limited-range simplicity and strong fresh food offers.

The major supermarkets are responding through loyalty schemes, price matching and promotions. Tesco continued to use Clubcard Prices to protect loyalty and defend against the discounters, while Sainsbury’s used Nectar Prices and its Aldi Price Match programme to reinforce value credentials.

M&S Food maintained momentum through premium convenience, food quality and smaller basket missions. The market is increasingly split between consumers looking for the lowest possible bill and those prepared to pay more for quality, convenience or a specific occasion.

Promotional activity remained elevated. Consumers have become accustomed to planning shops around offers, loyalty prices and multibuy deals. Full-price purchasing is harder to sustain, particularly in branded goods, while promotions have become a core part of how households manage food budgets.

Online grocery also remained an important source of growth with consumers using delivery and click and collect for larger planned shops, particularly around bank holiday weekends and family gatherings.

May also showed the continued strength of eating at home. Households are still using supermarkets to recreate restaurant occasions, buying premium ready meals, meal kits, desserts and drinks for socialising at home.

The warm weather supported this behaviour, with garden gatherings offering a lower-cost alternative to eating out.

Outlook

Summer should continue to support demand for barbecues, picnics, chilled drinks, convenience food and premium treats, particularly if warm weather persists. Major sporting events will also create further opportunities for retailers to capture spend linked to entertaining at home.

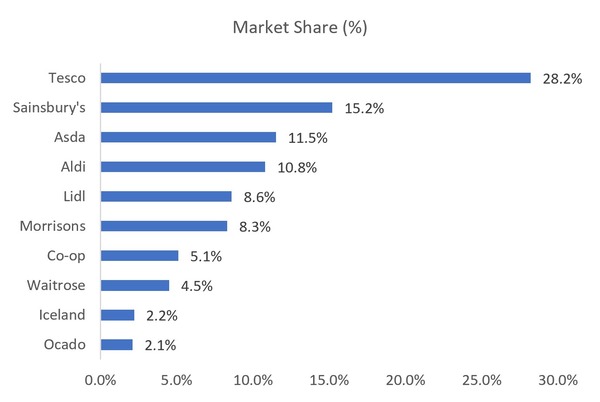

The competitive picture will remain intense. Lidl’s recent move ahead of Morrisons confirms that the discounters are still changing the market, forcing the major supermarkets to maintain heavy investment in loyalty pricing, price matching and promotions. Consumers are unlikely to abandon those habits quickly.

Food and grocery remains better placed than most retail categories as household budgets tighten. People cannot defer the weekly shop, but they can change what goes into the basket.

Take out a FREE 30 day membership trial to read the full report.

UK Grocery Market Share (12 weeks to 17 May)

Source: Worldpanel, Retail Economics

Source: Worldpanel, Retail Economics