Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Electricals sales

Electricals sales rose by xx% year-on-year in May, a substantial improvement on the xx% increase recorded in the same month last year. The result marked the strongest performance for the sector since November and reversed April’s Easter distorted decline.

Consumers also had a reason to spend in May, in anticipation for the summer of major sport. Televisions, sound systems and home entertainment were popular, while warmer weather supported demand for cooling products and some seasonal appliances.

May demonstrated that electricals can move quickly when a purchase has a purpose, a compelling promotion, or an immediate household need.

Key drivers and category performance

May’s recovery came from several sources at once: sport, weather, replacement demand and promotions. That mix makes the result more encouraging than a single event spike, even if demand for premium and non essential upgrades remains sensitive to household confidence.

Households preparing to watch football and other summer sport at home began upgrading televisions, soundbars and streaming equipment. Retailers used the period to bring forward promotional activity, giving consumers a reason to replace older products before the tournament calendar kicked off.

The heat also changed the product mix. Fans, air treatment products and cooling appliances were in demand as temperatures rose in the second half of the month.

Retailer updates point to improving conditions. AO has also seen demand improve across major domestic appliances, helped by its delivery proposition and customer service offer.

Underlying environment

May gave households some breathing room. Inflation held at xx%, grocery inflation eased to a 17-month low and oil prices fell from the levels seen earlier in the spring. Consumer confidence rose for the first time in four months, helping to support spending on products that had been deferred.

The improvement sat beside continued caution around bigger spending commitments. GfK’s Major Purchase Index fell to its lowest level since January 2025, showing that households remained wary of taking on expensive purchases without a notable reason.

A broken washing machine or an ageing television ahead of a major tournament can prompt a purchase, while premium upgrades without a distinct trigger are easier to postpone.

Interest rates stayed at xx% and mortgage rates edged higher, keeping pressure on household budgets. The labour market also cooled, with vacancies falling and wage growth easing.

Housing activity provides a secondary source of demand, especially for appliances. Mortgage approvals have improved in recent months, which should support sales linked to moves and renovations later in the year. For now, replacement cycles and event driven purchases remain more important to trading.

Outlook

Major sporting events should continue to support demand for televisions and audio, while further periods of hot weather could extend sales of cooling appliances.

The strength of that demand will depend heavily on price and availability. Consumers are still researching purchases and will continue to wait for deals, particularly on higher value products. Promotions, trade-in offers, finance and delivery promises will be important to conversion.

Take out a FREE 30 day membership trial to read the full report.

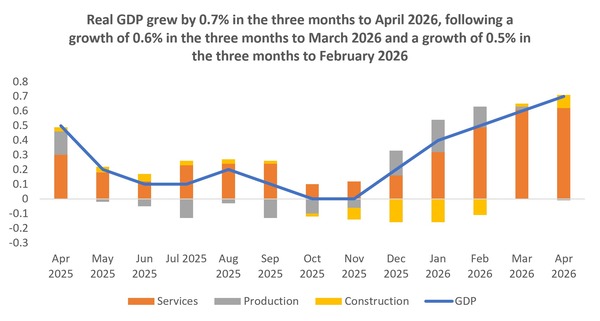

Real GDP grew by 0.7% in the three months to April 2026, following a growth of 0.6% in the three months to March 2026 and a growth of 0.5% in the three months to February 2026

Source: Retail Economics, ONS

Source: Retail Economics, ONS