UK Retail Sales Report summary

March 2026

Period covered: Period covered: 01 February - 28 February 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

Retail Sales Performance:

Retail sales lost momentum in February, with growth slowing to xx% year-on-year according to the Retail Economics Retail Sales Index, down from January’s sale-driven uplift.

Spending held up in food and health & beauty, while discretionary retail struggled to gain traction.

Factors impacting the headline performance in the month include:

Post-clearance slowdown: Heavy promotional activity in January pulled forward discretionary demand, leaving a quieter market once clearance activity faded. With confidence still fragile and fewer discounts in circulation, non-essential purchases fell back, particularly across fashion and home-related categories.

Weather disruption: February’s exceptionally wet conditions limited store traffic and delayed seasonal demand. Total footfall rose strongly from January levels but remained xx% below last year. Midweek footfall declined xx%, while weekends rose xx%, highlighting the shift towards more purposeful shopping trips.

Event-driven demand proved short-lived: Seasonal moments such as Valentine’s Day and half-term supported brief spikes in demand but did not shift the overall trajectory. Valentine’s Day drove stronger performance in categories such as jewellery, fragrance and premium dine-in grocery, with Worldpanel reporting £39m was spent on premium meal deals during the week. However, these effects were short-lived and insufficient to offset broader weakness.

Divergence across categories widened: Performance across retail categories remained uneven. Health and beauty and grocery continued to lead, supported by non-discretionary demand and smaller indulgences.

Clothing & footwear saw limited growth after January’s markdowns had brought forward spending. DIY & gardening and parts of the home market were held back by both weather and caution around larger purchases, while electricals remained mixed, with resilience in smaller-ticket items offset by weakness in big-ticket categories.

Category impact

Performance across retail categories remained uneven, with spending concentrated in essentials, wellbeing and smaller discretionary purchases, while demand for larger-ticket items stayed subdued.

Food and grocery remained the most dependable area, with sales rising xx% year-on-year. Growth continued to be driven by pricing, with own label, promotions and value ranges playing a central role.

Health and beauty (xx%) delivered one of the strongest performances of the month, outperforming the wider non-food market. The category continued to benefit from consistent demand linked to personal care, wellness routines and affordable indulgences.

Clothing and footwear had a more subdued month, with clothing sales rising xx% year-on-year, while footwear increased by just xx%. Poor weather and cautious spending delayed seasonal purchasing, limiting momentum after January’s clearance-driven uplift.

Electricals (xx) declined due to a mixed trading environment. Demand held up better for smaller-ticket and computing-related items, but this was not enough to offset continued weakness in big-ticket categories.

Furniture and flooring sales were broadly flat (xx%), as activity remained constrained by low transaction volumes in the housing market and ongoing reluctance to commit to higher-value purchases.

Homewares showed some resilience, with sales up xx% year-on-year. Performance was supported by smaller domestic upgrades and online demand.

DIY and gardening remained under pressure, with sales falling xx year-on-year. Adverse weather disrupted seasonal demand, while households continued to defer non-essential home projects.

Take out a FREE 30 day membership trial to read the full report.

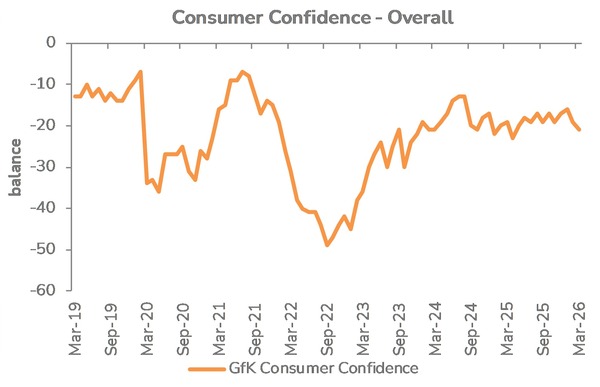

Confidence falls in February

Source: Retail Economics, GFK

Source: Retail Economics, GFK