UK Food & Grocery Sector Report summary

March 2026

Period covered: Period covered: 01 February - 28 February 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Food & Grocery Sales

Food and grocery sales rose by xx% year-on-year in February, ahead of the xx% increase recorded in the same month last year.

Growth remained driven primarily by pricing, with underlying volumes still under pressure as households continued to manage budgets tightly.

The category maintained its position as one of the more stable areas of retail, supported by essential demand and continued at-home consumption.

Key drivers and category performance

February continued to show price-led growth across grocery. Value growth tracked inflation which eased to xx% YoY, meaning a slight fall in unit volumes.

Promotional intensity increased further. A higher share of sales took place on promotion, and own-label penetration remained elevated as shoppers sought value. This shift supported volumes in lower-priced tiers while placing pressure on branded performance. Own label volumes increased xx%, while branded unit sales declined xx%, according to NIQ.

Consumer behaviour remained disciplined. Households focused on managing weekly spend, reducing waste and trading down where possible. Basket composition continued to adjust, with greater emphasis on staple categories and fewer discretionary items.

Event-led demand provided targeted support. Valentine’s Day drove an uplift in premium dine-in meal deals, with strong engagement in higher-quality own-label ranges.

Almost xx% of households bought a premium meal deal on Friday night ahead of Valentine’s Day (Worldpanel).

At-home consumption remained an important driver of performance. Ongoing caution around discretionary leisure spend, combined with poor weather, supported grocery demand, particularly in fresh, chilled and meal solution categories.

Online grocery continued to grow ahead of the market, supported by convenience and the expansion of rapid delivery services, particularly around the occasions during the month.

Food price surge?

Just over four weeks ago, the outlook for consumers and retailers was beginning to stabilise. Inflation was easing, rate cuts were expected, and there were early signs that pressure on household finances was starting to moderate.

The recent escalation in the Middle East has shifted the outlook for UK food prices, bringing cost pressures back into focus after a period of easing.

Higher oil and fuel costs feed into fertiliser, food production, packaging and distribution, with a lag before reaching retail prices.

Shipping disruption linked to Red Sea routes is adding further strain. Longer transit times, higher insurance costs and rerouting are pushing up import costs, particularly for ingredients and ambient goods. This creates uneven pressure across categories, with imported and energy-intensive products most exposed.

Retailers are entering this period with limited headroom. Labour, business rates and tax changes are already lifting operating costs, leaving less scope to absorb further increases. A greater share of cost pressure could therefore pass through to shelf prices over the coming quarters.

The Food and Drink Federation has indicated that food inflation could move higher again into 2026, with some forecasts pointing to high single-digit growth. Near-term data may remain relatively stable, but pressure is expected to build later in the year as costs feed through.

The political backdrop is tightening. Some grocers were cautious in early engagement with government due to concern over scrutiny of pricing, although a recent meeting with Rachel Reeves has been described as constructive.

Consumer behaviour is set to remain disciplined. Seasonal events and calendar moments will continue to provide short-term support, although these are likely to drive tactical trading up and not a consistent improvement in demand. Households are expected to maintain a strong focus on value, with continued growth in own-label penetration.

The operating environment will remain highly competitive, with success determined by pricing discipline, supply chain efficiency and the ability to respond to increasingly value-conscious consumer behaviour.

Take out a FREE 30 day membership trial to read the full report.

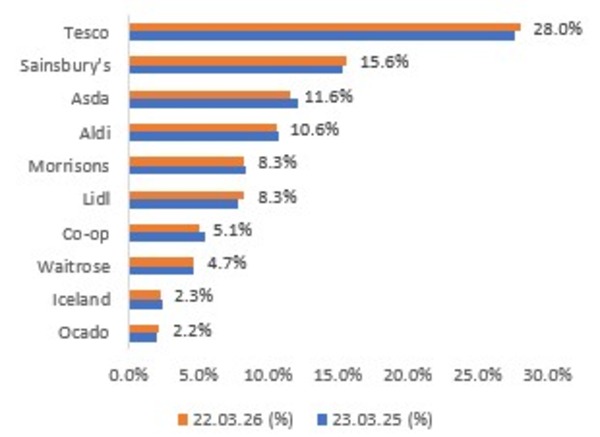

UK Grocery Market Share (12 weeks to 22 March)

Source: Kantar, Retail Economics

Source: Kantar, Retail Economics