UK Clothing & Footwear Sector Report summary

May 2026

Period covered: Period covered 05 April – 02 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

Clothing & Footwear Sales

Clothing and footwear sales weakened in April, with spending falling by xx% and xx% YoY, respectively. The category underperformed significantly relative to the same month last year, when clothing sales rose by xx% and footwear increased by xx%.

Easter timing distorted seasonal demand, with spring purchasing, occasionwear and gifting spend arriving earlier this year in March.

A combined March-April view offers a more reliable guide to underlying performance. Across the two-month period, clothing sales rose by xx%, well below the xx% increase recorded a year earlier, while footwear sales fell by xx%, against growth of xx% a year ago.

Key drivers

Last month’s warmer spell encouraged spring purchasing and occasionwear demand, providing an earlier boost to categories typically supported by seasonal change. By April, much of that spending had already occurred, reducing the need for additional purchases.

Clothing continues to benefit from relatively lower-ticket spending and frequent purchasing cycles, making it less vulnerable than larger discretionary categories. But consumers are increasingly focused on value, promotions and versatility, favouring practical wardrobe updates over more discretionary fashion purchases.

Footwear faced greater pressure. The category tends to be more discretionary, with purchases easier to postpone during periods of uncertainty.

Recent retailer commentary implies there’s an uneven performance across the market. Next’s recent trading update highlighted continued resilience, supported by strong online performance, marketplace growth and international demand. Yet the retailer has also warned that UK growth is likely to moderate in 2026 as favourable weather effects ease and consumer conditions become more difficult.

Macro backdrop

The economic backdrop became more challenging in April, increasing pressure on household budgets.

Rising fuel and energy prices linked to conflict in the Middle East pushed inflation concerns back into focus, reducing confidence just as households had expected greater financial relief.

Monetary policy expectations also shifted, with markets moving further away from expecting near-term interest rate cuts as policymakers responded cautiously to renewed inflation risks.

Consumer confidence around major purchases remained subdued, although clothing tends to hold up better than larger-ticket discretionary categories because of lower average transaction values and more frequent purchase cycles.

The labour market continues to offer some support; employment remains relatively stable and wage growth is still providing a degree of resilience for spending. But softer hiring demand and greater uncertainty around household finances will continue to encourage more cautious spending behaviour.

Next shields UK consumers from rising cost pressures

Next reported that it plans to offset some of the additional cost pressures arising from disruption in the Middle East through selective price increases in certain international markets, while keeping UK pricing broadly unchanged beyond the xx% increase already guided for this year. The move is expected to limit the immediate impact of higher freight and sourcing costs on UK consumers, with overseas markets absorbing a greater share of the adjustment.

Take out a FREE 30 day membership trial to read the full report.

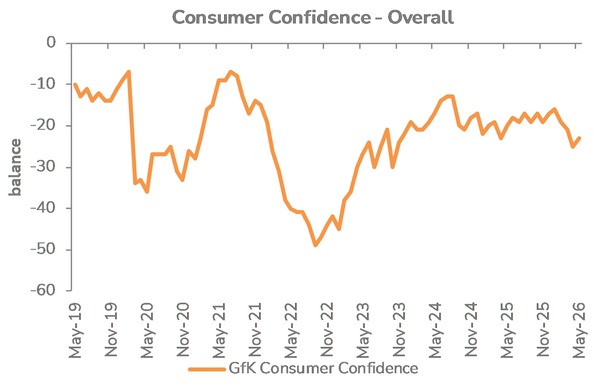

Consumer confidence edges up in May

Source: Retail Economics analysis, GFK

Source: Retail Economics analysis, GFK